I recently spent time with two friends, who happen to be financial advisors, where we discussed the proposed tax reform legislation and what it means for estate planning now and in the future. A link to the podcast is here.Enjoy listening! #estateplanning #legacyplanning #taxplanning #taxreform

In case you missed the virtual seminar this week on “Navigating Private Philanthropy During a Pandemic”, the recording can be found HERE and ask yourself, what will you do with your charitable dollars this year?

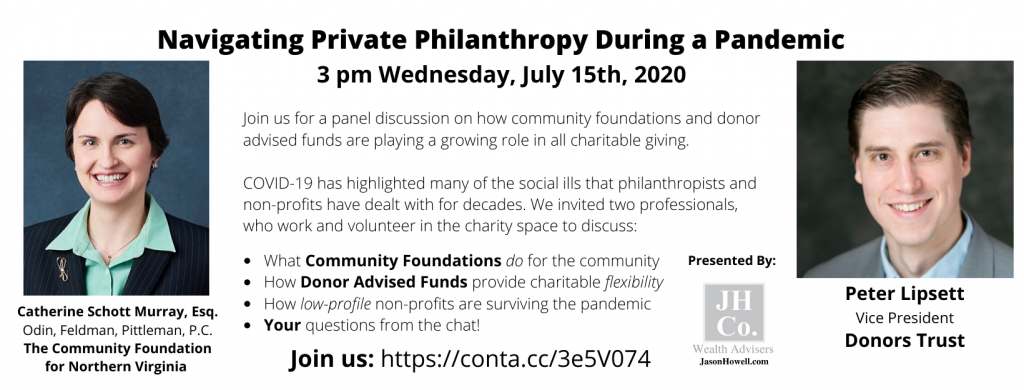

If you are looking to learn more about charitable giving and the options to engage in 2020, then please join me for a panel discussion on July 15, 2020 at 3:00 p.m. More information can be found here and below.

Businesses and individuals now will have until July 15th to file and pay their Federal income taxes. This means that you have an additional three months to plan and prepare your returns without having incurring penalties on up to $1 million in tax owed. Businesses will have the same period to pay amounts due on up to $10 million in tax owed. Learn more from attorney Catherine Schott Murray.

On March 18, 2020, the Families First Coronavirus Response Act was signed into law and will become effective not later than 15 days later, April 2, 2020. There are some differences between what was ultimately passed and what was summarized in our early article from March 16, 2020. Learn more from attorney Marina Blickley.

Construction and many other contractors who cannot telework may be receiving stop-work orders or facing other unique challenges on their government contracts in the face of COVID-19. Impacts may be exacerbated for personnel working in the field who may not be receiving guidance from the government due to unavailability of their Contracting Officers (CO) or Contracting Officer Representatives (COR). Learn more from attorney Shiva Hamidinia.

As the coronavirus shifts the way the world works, businesses should take this break in normal operating procedure to re-evaluate their finances. Learn more from attorney Brad Jones.

The end of the year is always a busy time of the year particularly in estate and tax planning. 2019 was no exception as on December 20th, the Setting Every Community Up for Retirement Enhancement Act (“the SECURE Act”) was signed into law. The SECURE Act took effect on January 1, 2020 and makes significant changes to qualified individual retirement account (“IRA”) planning, including the elimination of the stretch IRA for inherited IRAs, among other changes. Treasury Regulations have not yet been issued, so some of the details in the SECURE Act are still unknown and the gaps are not yet filled.

Before summarizing the elimination of the stretch IRA provisions, a few of the other key changes under the SECURE Act included the following:

The age for required minimum distributions (“RMDs”) to be drawn from retirement accounts is increased from 70 ½ to 72 years old.

The prohibition of retirement contributions after reaching 70 ½ is repealed.

Penalty-free withdrawals of up to $5,000 from retirement accounts to cover the costs of childbirth or adoption are permitted.

529 college savings plans can be used to cover the costs of apprenticeships and up to $10,000 can be withdrawn to help repay qualified student loans.

The pre-Tax Cuts and Jobs Act rates for the ‘kiddie tax’ is reinstated meaning that excess income will be taxed at a parent’s rate and not the trust and estate rates.

As mentioned, the most significant change under the SECURE Act is the elimination of the ability to stretch an inherited IRA (or 401(k) or 403(b)) with certain exceptions. The default rule now is that inherited IRAs must be fully distributed by the end of the 10th year following the death of the account owner. For example, if an account owner dies in 2020, leaving his or her IRA to a named beneficiary (who is not one of the defined exceptions), all monies from that IRA must be distributed by the end of 2030. The prior rule allowed beneficiaries to use their life expectancy to determine any required payout.

There are a few exceptions to this new default rule. Individuals who are permitted to stretch the inherited retirement account over their lifetime include:

The surviving spouse of the account holder.

A child of the account holder who has not yet reached the age of majority (in most jurisdictions, age 18). However, once the child reaches the age of majority, the default rule of 10 years kicks in.

Disabled individuals (which does include special needs trusts for such disabled individuals).

A chronically ill individual.

An individual who is not more than 10 years younger than the account holder.

The result of the new default rule for those who do not fall into an exempt category is that there will be less tax-deferred growth in the retirement account and an increase in income taxes because the rate of withdrawal has been accelerated.

There are some strategies available, which will be explained in more detail in later articles, that could help mitigate the increased tax liability. Those strategies include:

Qualified charitable distribution (“QCD”) – For those charitably inclined, an individual who is more than 70 ½ could make a gift directly to a charity by way of a QCD from his or her IRA. Such gifts are limited to $100,000 per year.

Charitable Remainder Trusts (“CRTs”) – Again for those charitably inclined, using a CRT may be an option to provide an income to a beneficiary during a specified time with a charity or charities receiving the remainder once the time period has passed.

Roth conversions – Much discussion is being had about individuals reviewing whether converting their tax-deferred IRAs to Roth IRAs is appropriate, which would alleviate the concern that beneficiaries will receive a huge tax bill.

Life insurance – Individuals may want to consider withdrawals from an IRA to pay premiums on a life insurance policy that instead could be left to their designated beneficiary tax free.

These strategies are heavily dependent on the specific circumstances faced by each IRA account holder and should be reviewed carefully.

Lastly, for many who have had their estate planning prepared, that plan may be structured around a revocable living trust with the revocable living trust being designated as the beneficiary of the IRA. As a result, those beneficiary designations and the terms of the trust need to be revisited as unintended income tax consequences may result because of the new 10 year default payout rule.

As for next steps, if you haven’t reviewed your beneficiary designations and your estate plan recently, you should consult with your team of professional advisors who can help explore the options available to you based on your situation. #estateplanning #SECUREAct #taxplanning @bgnthebgn @OFPLAW

(h/t to my colleague,David A. Lawrence, Esq. who recently attended the Annual Virginia Tax Roundtable and provided the summary below.)

It’s time, once again, to share some of the tidbits that I gleaned from

the Annual Virginia Tax Roundtable. Each year, a small group of

Virginia tax lawyers convenes to meet with the Virginia Tax

Commissioner, his staff, and the Attorney General’s staff to talk about

what the Tax Department is thinking, the challenges that they are

facing, and ideas for improved tax administration in Virginia.

In addition to responding to changes ushered in by the 2017 Tax Act, Virginia taxpayers and tax preparers should take note of several new and existing factors that could complicate your tax filing efforts.

Identity Theft & Refund Fraud Continues at High Levels

The

rise in fraudulent refund filings remains a big issue for the Tax Department,

and the additional scrutiny required to identify those cases continue to slow

processing of Virginia tax returns. The

good news: the Department believes it is

catching more of these fraudulent filings before checks are issued; it denied

more than $32 million in fraudulent 2017 refunds just through October 21, 2018

of this year.

More Retirements & Staffing Challenges

The

State is continued to be challenged by the retirements of long experienced tax

examiners, and they are trying to hire new examiners as quickly as

possible. Particularly hard hit has been

compliance field audit personnel in Northern Virginia and Tidewater.

Audit Focuses

Speaking

of audits, the Tax Department engaged an outside consultant to help it be more

proactive in its compliance and audit activities. It is considering expanding reviews of

Schedule A deductions and Schedule C deductions. Further, the agency has lots of federal

return data, as well as data from other federal programs. Now, according to the Commissioner, the state

just needs a better, more efficient way to use that data for compliance and

audits. Note that fewer appeals are

coming to the Tax Department, and the Tax Department particularly hates dealing

with tax appeals from local jurisdictions.

2017 Tax Act – A Great Revenue Windfall for Virginia

The

changes made by the federal 2017 Tax Legislation are projected to give a

windfall of additional tax revenue to Virginia from individual filers. The General Assembly loves the extra revenue,

as long as it is not blamed for raising taxes.

There may be some proposals this year in the General Assembly to

increase Virginia’s standard deduction, increase the personal exemption, and/or

permit Virginia itemizing for an individual even if that individual took the federal

standard deduction. There have not been

many inquiries from the Legislature to the Tax Commissioner on the business

side of the 2017 Tax Act. It is expected

that some type of federal conformity, with exceptions, will be in place by mid-February

2019 effective for 2018 and onward.

One

of the biggest windfalls for the State is the fact that if more individuals use

the federal standard deduction, they are currently required to use the Virginia

standard deduction, which is very low.

Furthermore, for those who do itemize, the repeal and limitation of

those itemizable deductions also produces more revenue for Virginia. Finally, the limitations on loss deductions,

net interest deductions, and NOL deductions produce additional revenue for

Virginia. On the other hand, Virginia

loses revenue with the increased Section 179 Expensing and the fact that more

“small” businesses will be able to use the cash method of accounting.

Registering with the SCC Triggers Virginia Tax Filings for Businesses

The

Department confirmed that if a non-Virginia corporation or entity registers

with the Virginia SCC as a foreign entity, it automatically must start filing

Virginia income tax returns, even if it has no income.

Non-Resident Rulings

The

Department keeps pumping out lots of rulings on Virginia residents versus

non-residents for taxation purposes.

They are all fact specific, and make it difficult for former residents

to be treated as non-Virginia tax residents when they continue to maintain ties

to Virginia after they have left the state (particularly if they try to leave

the State just prior to the year in which a large sale transaction occurs).

A Brave New World in Collecting Sales Tax from Out of State Businesses – the Wayfair Decision

The

U.S. Supreme Court’s decision in Wayfair this past year effectively overturned

the requirement for “physical presence” in order for a state to subject nonresident

businesses to collect sales taxes for other states.

As

a result of the Court’s decision, if a business had a physical presence in a state,

then that state may still require that business to collect and pay sales tax on

sales made into that state. Additionally,

states that have statutes similar to the one at issue in Wayfair, where an out-of-state

business has numerous sales into a state (either in raw numbers of transactions

or in the amount of dollars), then that state may now require those out-of-state

sellers to collect and pay sales tax on sales made into that state.

Virginia

has not acted yet to implement the Wayfair decision, but most other states have

acted with various thresholds. This

revenue raiser will likely be added to this coming General Assembly’s

legislative calendar. As an example of

taxable nexus, the Wayfair situation subjected a company to collect and pay

sales taxes to a state where the company had either at least $100k in sales or

at least 200 transactions in that State.

This will have a big impact on internet sellers, software sellers, and other “free shipping” product sales. A future question raised by the Wayfair case is whether states will try to use it to expand that ruling into the income tax and local tax area. The Supreme Court used old “income tax” nexus cases as part of its logic in support of the Wayfair decision. So expect more to come.

Documentation filed earlier this week in Oakland County probate court in Michigan by Aretha Franklin’s children indicates that she died without a will or a trust. On the forms, a box was checked signaling that “the decedent died intestate”. What does this all mean?

Dying without a Last Will and Testament or a revocable living trust means that a person is intestate and the laws of the state in which they resided at death will spell out who is to receive the assets of the estate. Under Michigan law, Ms. Franklin’s estate will pass equally to her children as she was unmarried at the time of her death. Ms. Franklin’s niece has also requested that she be appointed as the personal representative or executor of the estate. Thus, it appears that the law of unintended consequences may now apply as Ms. Franklin may not have wanted her children to become the beneficiaries. She may have wanted to include charity or friends perhaps even other relatives in her estate plan. She may not have wanted to have her niece serve as the personal representative, a role that presumably will be compensated. But, without a Last Will and Testament or revocable living trust, we will never know what her true wishes were.

It will also be interesting to see how the administration of Ms. Franklin’s estate unfolds now that the process will be a public one. A number of questions will have to be asked and answered, including, but not limited to: What debts does the singer have? Michigan may not have a state level estate tax or inheritance tax, but how will the Federal estate tax be paid? Exemptions from Federal estate tax are high ($11.18 million per person in 2018), and valuations of Ms. Franklin’s will have to be done to determine the total value of her estate. What assets will each beneficiary ultimately receive? Presumably some of the assets are not standard such as royalties from Ms. Franklin’s records. Will an agreement be reached amongst the beneficiaries regarding the management and distribution of the assets? Unfortunately, the process that has begun will be lengthy, likely expensive and could result in the dismantling of a legacy if the process devolves into an ugly court battle similar to what has happened with Prince’s estate when he died without a will. And in the end, all of this uncertainty could have been avoided or at least minimized had Ms. Franklin simply planned, which means “you better think” before you decide you do not need a plan. #QueenofSoulDiesWithoutWill #QueenofSoul #estateplanning #intestacy

Welcome to the New Year! As with any new year, there are usually changes to a variety ofimportant numbersfor estate planning and elder law purposes. This year the applicable exclusion amount from Federal estate tax is set at $11.18 million per person thanks totax reform. The lifetime exclusion from gift tax is also $11.18 million per person and the exemption from generation skipping transfer tax is $11.18 million. The annual exclusion from gift tax will be at least $14,000.

For local jurisdictions that have estate tax, the District of Columbia increased its estate tax exemption from $1,000,000 to $2,000,000 last year and this year has increased the threshold further to match the Federal exemption. Maryland’s exemption from estate tax has increased to $4,000,000. Virginia continues to have no state level estate or inheritance tax.

In the elder law field, theMedicaidspousal impoverishment numbers were released increasing the minimum community spouse resource allowance (CSRA) to $24,720 and the maximum CSRA to $123,600. The maximum monthly maintenance needs allowance is now $3,090.00 while the minimum remains at $2,030.00. The minimum home equity limit is now $572,000 and the maximum is $858,000, but be aware that local jurisdictions may apply these limits differently.

If you have questions regarding the new limits and how they may impact your estate planning, your should consult your professional advisor. #estateplanning #taxplanning #elderlaw #taxreform #HappyNewYear @bgnthebgn

As the year draws to an end, many of you look to make your charitable donations or are advising individuals regarding their charitable donations. Of course, there are a variety of ways in which one can make such a charitable gift. The IRS recently published IR 2017-191, which is part of a series of articles providing taxpayers with relevant information so they can be ready for the next tax season. In this recent article, the IRS reminded taxpayers of certain aspects of charitable giving in an effort to help taxpayers avoid problems come tax time. I have summarized these helpful tips below.

For starters, individuals can only receive a tax deduction if the charity to which they donate is an ‘eligible organization.’ The IRS has a website,Select Check, that is a searchable online database of ‘eligible organizations’ that can be used to verify the status of an organization.

Next, charitable donations can only be deducted if the taxpayer itemizes their deductions. For some this can be a hassle because that means maintaining accurate records and receipts. If the gift is larger than $250 to the charity, then a written acknowledgement is required. The IRS has providedPublication 526on charitable contributions to help explain what records are necessary.

Additionally, if an individual is looking to donate tangible personal property like clothing or household items, those items have to be in ‘good used or better’ condition. Household goods include furniture, furnishings, electronics, appliances and linens. The taxpayer must obtain a detailed receipt in which the donated items are described for donations worth $250 or more. Items in which a deduction of more than $500 is claimed usually have to include a qualified appraisal.

Another factor to keep in mind is if the taxpayer receives any ‘benefit’ in the form of merchandise, meals, tickets or other items. The value of such ‘benefit’ will reduce the available deduction amount. For example, a contributor membership to the Kennedy Center is valued at $120, but only $80 of that amount is eligible to be deducted.

One alternative to keeping lots of records and receipts from every organization is the creation of a donor advised fund. An individual can make a single larger contribution to his or her donor advised fund and from that donor advised fund make specific charitable donations. There are a variety of terms and conditions to follow, but the single contribution means that is what is reported on one’s tax returns.Hereis just one person’s rationale behind the creation of a donor advised fund that also allowed her to get more involved with her community.

Ultimately, any gift is welcomed by the charity and you should feel free to reach out to the charity or your professional advisor if you have questions or need assistance in making year-end charitable donations. #GivingTuesday @CFNOVA @bgnthebgn #donoradvisedfunds #taxplanning #charitablegiving

A year ago Treasury proposed new regulations to Section 2704 of the Internal Revenue Code that would significantly reduce or eliminate the ability to use valuation discounting in certain transactions where business interests are transferred. The proposed regulations would mean that the parties to those types of transactions could incur estate or gift tax. Towards the end of last year, a public hearing on the regulations was held in which many expressed concerns about how these proposed regulations would impact small businesses and the like. However, at the time the future of the regulations was unknown given the change of administration,

Earlier this year, the President issued Executive Order 13789 in which the President instructed Treasury to review all “significant tax regulations” and identify those regulations that (a) impose an undue financial burden, (b) add undue complexity to our tax laws, and (c) exceed statutory authority of the IRS. Treasury issued Notice 2017-38 in which the proposed regulations to Section 2704 were identified as meeting these criteria. A comment period followed the issuance of the Order and has now closed. During the comment period, a study was submitted by The S Corporation Association that showed the detrimental impact of such regulations should they be finalized. A final report is due to the President within the next month that is to suggest possible reforms to the identified regulations ranging from modification to the regulations to a full appeal. Until the future is certain, valuation discounting remains available. #valuationdiscounts #2704regulations #businessvaluations #estateplanning #businessplanning @bgnthebgn

Documentation filed earlier this week in

Documentation filed earlier this week in

As the year draws to an end, many of you look to make your charitable donations or are advising individuals regarding their charitable donations. Of course, there are a variety of ways in which one can make such a charitable gift. The IRS recently published

As the year draws to an end, many of you look to make your charitable donations or are advising individuals regarding their charitable donations. Of course, there are a variety of ways in which one can make such a charitable gift. The IRS recently published  A year ago Treasury

A year ago Treasury