Click here to learn more.

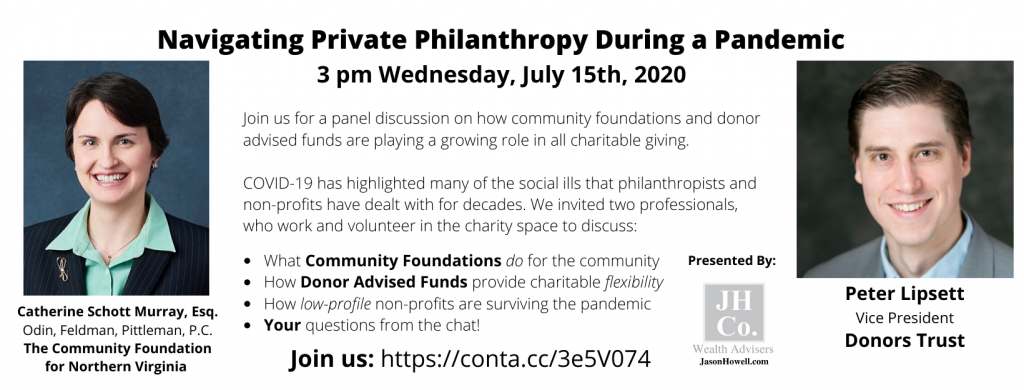

In case you missed the virtual seminar this week on “Navigating Private Philanthropy During a Pandemic”, the recording can be found HERE and ask yourself, what will you do with your charitable dollars this year?

If you are looking to learn more about charitable giving and the options to engage in 2020, then please join me for a panel discussion on July 15, 2020 at 3:00 p.m. More information can be found here and below.

As the year draws to an end, many of you look to make your charitable donations or are advising individuals regarding their charitable donations. Of course, there are a variety of ways in which one can make such a charitable gift. The IRS recently published IR 2017-191, which is part of a series of articles providing taxpayers with relevant information so they can be ready for the next tax season. In this recent article, the IRS reminded taxpayers of certain aspects of charitable giving in an effort to help taxpayers avoid problems come tax time. I have summarized these helpful tips below.

As the year draws to an end, many of you look to make your charitable donations or are advising individuals regarding their charitable donations. Of course, there are a variety of ways in which one can make such a charitable gift. The IRS recently published IR 2017-191, which is part of a series of articles providing taxpayers with relevant information so they can be ready for the next tax season. In this recent article, the IRS reminded taxpayers of certain aspects of charitable giving in an effort to help taxpayers avoid problems come tax time. I have summarized these helpful tips below.

For starters, individuals can only receive a tax deduction if the charity to which they donate is an ‘eligible organization.’ The IRS has a website, Select Check, that is a searchable online database of ‘eligible organizations’ that can be used to verify the status of an organization.

Next, charitable donations can only be deducted if the taxpayer itemizes their deductions. For some this can be a hassle because that means maintaining accurate records and receipts. If the gift is larger than $250 to the charity, then a written acknowledgement is required. The IRS has provided Publication 526 on charitable contributions to help explain what records are necessary.

Additionally, if an individual is looking to donate tangible personal property like clothing or household items, those items have to be in ‘good used or better’ condition. Household goods include furniture, furnishings, electronics, appliances and linens. The taxpayer must obtain a detailed receipt in which the donated items are described for donations worth $250 or more. Items in which a deduction of more than $500 is claimed usually have to include a qualified appraisal.

Another factor to keep in mind is if the taxpayer receives any ‘benefit’ in the form of merchandise, meals, tickets or other items. The value of such ‘benefit’ will reduce the available deduction amount. For example, a contributor membership to the Kennedy Center is valued at $120, but only $80 of that amount is eligible to be deducted.

One alternative to keeping lots of records and receipts from every organization is the creation of a donor advised fund. An individual can make a single larger contribution to his or her donor advised fund and from that donor advised fund make specific charitable donations. There are a variety of terms and conditions to follow, but the single contribution means that is what is reported on one’s tax returns. Here is just one person’s rationale behind the creation of a donor advised fund that also allowed her to get more involved with her community.

Ultimately, any gift is welcomed by the charity and you should feel free to reach out to the charity or your professional advisor if you have questions or need assistance in making year-end charitable donations. #GivingTuesday @CFNOVA @bgnthebgn #donoradvisedfunds #taxplanning #charitablegiving

As the year draws to an end, many of you look to make your charitable donations or are advising individuals regarding their charitable donations. Of course, there are a variety of ways in which one can make such a charitable gift. The IRS recently published IR-2016-154, which is part of a series of articles providing taxpayers with relevant information so they can be ready for the next tax season. In this recent article, the IRS reminded taxpayers of certain aspects of charitable giving in an effort to help taxpayers avoid problems come tax time. I have summarized these helpful tips below.

As the year draws to an end, many of you look to make your charitable donations or are advising individuals regarding their charitable donations. Of course, there are a variety of ways in which one can make such a charitable gift. The IRS recently published IR-2016-154, which is part of a series of articles providing taxpayers with relevant information so they can be ready for the next tax season. In this recent article, the IRS reminded taxpayers of certain aspects of charitable giving in an effort to help taxpayers avoid problems come tax time. I have summarized these helpful tips below.

For starters, individuals can only receive a tax deduction if the charity to which they donate is an ‘eligible organization.’ The IRS has a website, Select Check, that is a searchable online database of ‘eligible organizations’ that can be used to verify the status of an organization.

Next, charitable donations can only be deducted if the taxpayer itemizes their deductions. For some this can be a hassle because that means maintaining accurate records and receipts. If the gift is larger than $250 to the charity, then a written acknowledgement is required. The IRS has provided Publication 56 on charitable contributions to help explain what records are necessary.

Additionally, if an individual is looking to donate tangible personal property like clothing or household items, those items have to be in ‘good used or better’ condition. Household goods include furniture, furnishings, electronics, appliances and linens. The taxpayer must obtain a detailed receipt in which the donated items are described for donations worth $250 or more. Items in which a deduction of more than $500 is claimed usually have to include a qualified appraisal.

Another factor to keep in mind is if the taxpayer receives any ‘benefit’ in the form of merchandise, meals, tickets or other items. The value of such ‘benefit’ will reduce the available deduction amount. For example, a contributor membership to the Kennedy Center is valued at $120, but only $80 of that amount is eligible to be deducted.

One alternative to keeping lots of records and receipts from every organization is the creation of a donor advised fund. An individual can make a single larger contribution to his or her donor advised fund and from that donor advised fund specific charitable donations can be made. There are a variety of terms and conditions to follow, but the single contribution means that is what is reported on one’s tax returns. Here is just one person’s rationale behind the creation of a donor advised fund that also allowed her to get more involved with her community.

Ultimately, any gift is welcomed by the charity and you should feel free to reach out to the charity or your professional advisor if you have questions or need assistance in making year-end charitable donations. @CFNOVA @bgnthebgn #donoradvisedfunds #taxplanning #charitablegiving

As another year begins many individuals make resolutions. Very often one of those resolutions is to have an estate plan prepared or update an outdated estate plan. A couple of considerations in preparing an estate plan is whether you are charitably inclined and would you like to do more for your community? A donor advised fund is one way to set aside funds for charitable purposes that can be capitalized upon during your lifetime and within your estate plan. Moreover, a donor advised fund can continue after you are gone. Here is just one person’s rationale behind the creation of a donor advised fund that also allowed her to get more involved with her community. @CFNOVA #donoradvisedfunds #taxplanning #charitablegiving