Recently, I sat down with the National Cemetery Administration to discuss how legal advisers can help veterans and their families make informed decisions during the estate planning process.

The video, “A Simple Question. A Clear Advantage — What Estate and Financial Plans Overlook,” highlights the veterans’ burial and memorial benefits that many overlook because they lack awareness.

During this time of year as families gather for the holidays, it is important to gain clarity as to the wishes of your parents in order to protect their legacy. Check out this podcast in which members of Monument Wealth Management and I discuss how best to approach the conversation of incapacity and dying. #estateplanning #incapacityplanning

In May, I sat down with Jason Howell to discuss the process of estate planning and why it is important that families “begin the begin”. Check out the podcast/video recording of our time together. #estateplanning #incapacityplanning #beginthebegin

I recently spent time with two friends, who happen to be financial advisors, where we discussed the proposed tax reform legislation and what it means for estate planning now and in the future. A link to the podcast is here.Enjoy listening! #estateplanning #legacyplanning #taxplanning #taxreform

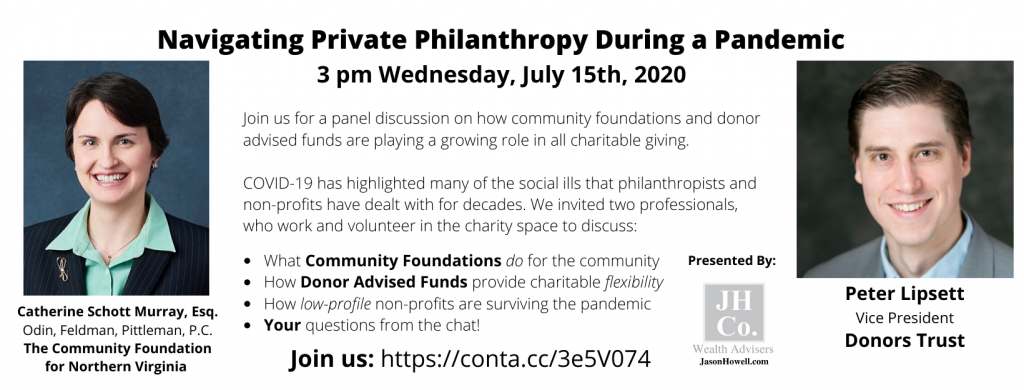

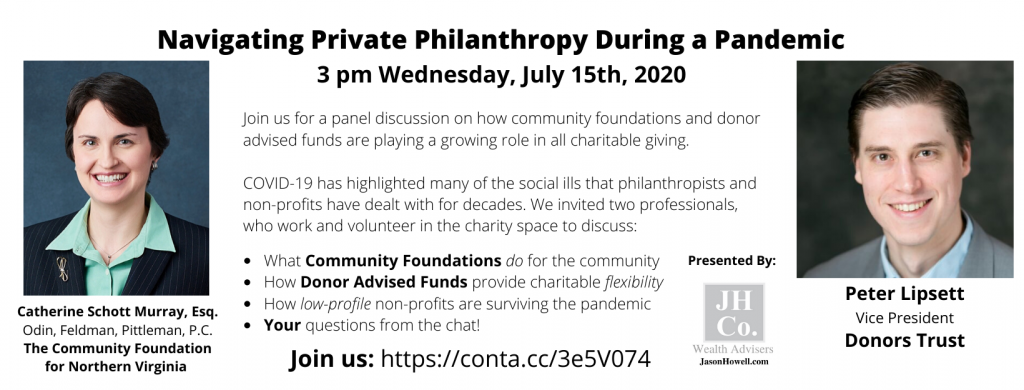

In case you missed the virtual seminar this week on “Navigating Private Philanthropy During a Pandemic”, the recording can be found HERE and ask yourself, what will you do with your charitable dollars this year?

If you are looking to learn more about charitable giving and the options to engage in 2020, then please join me for a panel discussion on July 15, 2020 at 3:00 p.m. More information can be found here and below.

Businesses and individuals now will have until July 15th to file and pay their Federal income taxes. This means that you have an additional three months to plan and prepare your returns without having incurring penalties on up to $1 million in tax owed. Businesses will have the same period to pay amounts due on up to $10 million in tax owed. Learn more from attorney Catherine Schott Murray.

On March 18, 2020, the Families First Coronavirus Response Act was signed into law and will become effective not later than 15 days later, April 2, 2020. There are some differences between what was ultimately passed and what was summarized in our early article from March 16, 2020. Learn more from attorney Marina Blickley.

Construction and many other contractors who cannot telework may be receiving stop-work orders or facing other unique challenges on their government contracts in the face of COVID-19. Impacts may be exacerbated for personnel working in the field who may not be receiving guidance from the government due to unavailability of their Contracting Officers (CO) or Contracting Officer Representatives (COR). Learn more from attorney Shiva Hamidinia.

As the coronavirus shifts the way the world works, businesses should take this break in normal operating procedure to re-evaluate their finances. Learn more from attorney Brad Jones.

Out of an abundance of caution and with the utmost respect for our seniors and their caregivers, we have postponed the launch of our upcoming series, Real Talk: The Essentials of Aging with Confidence, until further notice.

We hope to proceed with our April session if it is prudent to do so. Be sure to watch for more information in the coming weeks.

This month we begin the first of a 3-part series in which we tackle topics involving The Essentials of Aging with Confidence. Details below including where to register. We look forward to seeing you there!

March 18th – Part 1: Getting Your Estate in Order April 22nd – Part 2: Aging in Place or Assisted Living? Which option works for your lifestyle? May 13th – Part 3: The Essential Guide to Aging and Caregiving. @bgnthebgn @ofplaw @sandyspringbank #shepherdscenter #agingwithconfidence

The end of the year is always a busy time of the year particularly in estate and tax planning. 2019 was no exception as on December 20th, the Setting Every Community Up for Retirement Enhancement Act (“the SECURE Act”) was signed into law. The SECURE Act took effect on January 1, 2020 and makes significant changes to qualified individual retirement account (“IRA”) planning, including the elimination of the stretch IRA for inherited IRAs, among other changes. Treasury Regulations have not yet been issued, so some of the details in the SECURE Act are still unknown and the gaps are not yet filled.

Before summarizing the elimination of the stretch IRA provisions, a few of the other key changes under the SECURE Act included the following:

The age for required minimum distributions (“RMDs”) to be drawn from retirement accounts is increased from 70 ½ to 72 years old.

The prohibition of retirement contributions after reaching 70 ½ is repealed.

Penalty-free withdrawals of up to $5,000 from retirement accounts to cover the costs of childbirth or adoption are permitted.

529 college savings plans can be used to cover the costs of apprenticeships and up to $10,000 can be withdrawn to help repay qualified student loans.

The pre-Tax Cuts and Jobs Act rates for the ‘kiddie tax’ is reinstated meaning that excess income will be taxed at a parent’s rate and not the trust and estate rates.

As mentioned, the most significant change under the SECURE Act is the elimination of the ability to stretch an inherited IRA (or 401(k) or 403(b)) with certain exceptions. The default rule now is that inherited IRAs must be fully distributed by the end of the 10th year following the death of the account owner. For example, if an account owner dies in 2020, leaving his or her IRA to a named beneficiary (who is not one of the defined exceptions), all monies from that IRA must be distributed by the end of 2030. The prior rule allowed beneficiaries to use their life expectancy to determine any required payout.

There are a few exceptions to this new default rule. Individuals who are permitted to stretch the inherited retirement account over their lifetime include:

The surviving spouse of the account holder.

A child of the account holder who has not yet reached the age of majority (in most jurisdictions, age 18). However, once the child reaches the age of majority, the default rule of 10 years kicks in.

Disabled individuals (which does include special needs trusts for such disabled individuals).

A chronically ill individual.

An individual who is not more than 10 years younger than the account holder.

The result of the new default rule for those who do not fall into an exempt category is that there will be less tax-deferred growth in the retirement account and an increase in income taxes because the rate of withdrawal has been accelerated.

There are some strategies available, which will be explained in more detail in later articles, that could help mitigate the increased tax liability. Those strategies include:

Qualified charitable distribution (“QCD”) – For those charitably inclined, an individual who is more than 70 ½ could make a gift directly to a charity by way of a QCD from his or her IRA. Such gifts are limited to $100,000 per year.

Charitable Remainder Trusts (“CRTs”) – Again for those charitably inclined, using a CRT may be an option to provide an income to a beneficiary during a specified time with a charity or charities receiving the remainder once the time period has passed.

Roth conversions – Much discussion is being had about individuals reviewing whether converting their tax-deferred IRAs to Roth IRAs is appropriate, which would alleviate the concern that beneficiaries will receive a huge tax bill.

Life insurance – Individuals may want to consider withdrawals from an IRA to pay premiums on a life insurance policy that instead could be left to their designated beneficiary tax free.

These strategies are heavily dependent on the specific circumstances faced by each IRA account holder and should be reviewed carefully.

Lastly, for many who have had their estate planning prepared, that plan may be structured around a revocable living trust with the revocable living trust being designated as the beneficiary of the IRA. As a result, those beneficiary designations and the terms of the trust need to be revisited as unintended income tax consequences may result because of the new 10 year default payout rule.

As for next steps, if you haven’t reviewed your beneficiary designations and your estate plan recently, you should consult with your team of professional advisors who can help explore the options available to you based on your situation. #estateplanning #SECUREAct #taxplanning @bgnthebgn @OFPLAW